If you want to go heavy duty into it I recommend the Hull book (options, futures and other derivatives) but for your purposes the investopedia articles are enough.

Basically naked puts means you’re selling downside insurance so if the stock crashes you eat the loss. Covered calls mean you sell upside risk but have the stock so if it goes up you make a little.

Hull is a great book and is not too heavy on the math. However, for someone just getting their feet wet, Options as a Strategic Investment by MacMillan is a classic.

The "tail" in tail risk referes to the tails of a probability distribution. A normal distribution has "thin" tails. The probability of huge outliers is pretty low.

If you have tail risk, then it means you have a decent chance of losing a lot more money than the typical variation. Your returns might look like +1.1, +0.9, +1.2 +1.05, -3. So your profit is pretty predictable with little variation, until suddenly you lose a lot of money.

The only book you should read is John Bogel's. Do what he says like Goldman partners, Bank of America senior executives, almost every economist does with their money and stick it in low cost diversified mutual funds.

Or you can learn stochastic calculus and end up in the same place once you realize half of all active traders do worse than the market, before fees.

None of the kinds of people you listed are good at trading (esp economists). From experience, professional traders do tend to use passive indices for part of their PA, but also actively trade a portion.

But you're right in that if you don't have a passion for it, you'll never be able to truly outperform spy on a risk adjusted basis. However, if you do have the knowledge and the passion, I definitely think you can.

Investing is personal, and just holding spy doesn't fulfill everyone's objectives.

Here's an example of a strategy that outperforms spy in most cases: 1/3 of your portfolio goes to upro (3x leveraged spy) and 2/3s goes to a bond fund/etf. As long as the bond etf returns above the upro expense ratio (~1%), you will outperform. From my backtests, this strategy will earn you an extra 1-2% return a year, while also having a slightly higher risk adjusted returns.

I list the above as a great example because it's the kind of strategy that is great for a PA: easy to manage, doesn't require babysitting, and backed by solid academic research. When people think active vs passive, they think actively trading single stocks vs just holding an index. My point is that you can use some quant-lite strategies that tilt your portfolio to eek out a little return. You don't have to be trading everyday or even holding anything except ETFs.

While I always preached just buying the S&P one risk i've been seeing with it is if, a majority of investors just buy the S&P index, since the index is market cap weighted, it would just make the largest stocks in the index more expensive.

This would make the stocks that have less weight in the index or stocks outside the index relatively cheap and obviously offer better returns.

Assuming the amount of tradable shares for each stock is proportional to the free float capitalization (which is not a particularly good assumption), each stock in the index should be pushed up by the same amount, since the weight of each stock in the index is proportional to the market cap of the stock. I don't think this is actually true (i.e the number of shares on the market is not proportional to the market cap), which would imply that some share prices would be affected more than other. Do higher weight stocks in spy get pushed up more? I don't know. But it is certainly possible.

With respect to the stocks just outside the index, I think you could argue that they are probably undervalued and thus should offer better returns. This is what an academic would say. However, the actual reality could be a lot different: if returns are dominated by flows instead of fundamentals (like they are now), maybe going with the crowd is the best investment strategy. Or maybe not, I haven't done the research.

One thing that every market professional is worried about right now is just how dysfunctional valuations and returns seem to be in the modern era. Stocks seem to go up for no reason and returns have been disconnected from both fundamental and quantitative risk premia.

What I can say for sure is that we are in a period of intense change in the financial system. No one knows what the future of finance will look like, 10 years, 20, or 30 years out. Will crypto defi take over? Will traditional finance be disrupted? No one knows, but it is certainly an exciting time to work in the capital markets!

Sorry, I'm using risk premia incorrectly (quant equities isn't actually my thing).

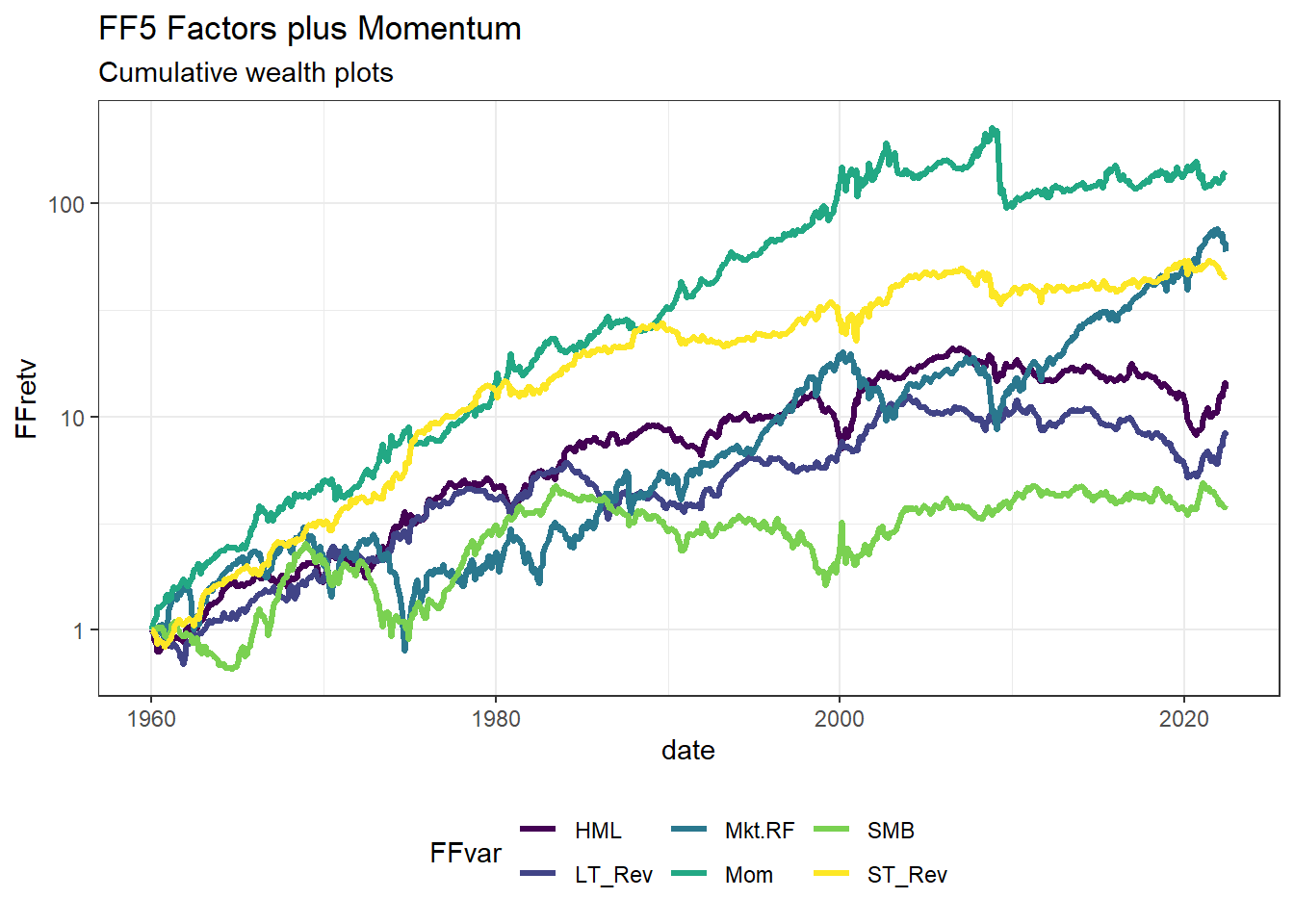

What I mean is that I don't believe smb truly delivers superior risk adjusted returns. For example, I believe the betting against beta factor (BAB) does, while smb does not.

We agree then, the size factor has not been really outperforming since it was introduced in the nineties. Maybe the drivers of the outperformace were things like transaction costs and lack of information which are less of an issue in recent times.

For what it’s worth, the value factor is not doing well recently either...

by beta slippage you mean volatility drag? On a risk adjusted basis, upro is definitely a loser due to volatility drag and high expense ratio. However, you can easily calculate optimal leverage ratio in order to maximize the geometric growth of your portfolio. The equation is:

lev = E(r) / Var(r)

So if the expected return is 10% and the expected volatility is 10%, optimal leverage to maximize geometric growth is 10x.

This of course is much too high and the risk of losing everything due to excessive kurtosis and downside skew is very high. Like the everything else in finance, fundamental sin of that formula is assumption of the log normality of returns.

However, is 3x too high for the long term? I dunno, but over long time periods, a pure 3x leveraged spy portfolio is going to outperform significantly. The problem is most people will be unable to weather the storm as you can easily lose half of your money in a week.

I wouldn't hold pure spy 3x and wouldn't exactly recommend it, but from a mathematical perspective it is a defensible (as in, you can make cogent arguments for it) long term investment.

On the other hand, I would probably recommend 1.5x lev or possibly even 2x lev to certain people.

As a quant, I approach these things like leverage from a mathematical perspective. It's important not to have an emotional reaction. There are very smart people running books that have 10x leverage but you would never be able to guess by looking at their volatility. It's all about the factor exposures, net delta, etc.

For example I've seen 15x leveraged delta neutral books that have absolutely insane Sharpe ratios (>15) and annualized volatility of less than 5%.

> However, is 3x too high for the long term? I dunno, but over long time periods, a pure 3x leveraged spy portfolio is going to outperform significantly. The problem is most people will be unable to weather the storm as you can easily lose half of your money in a week.

You don't define "long time periods" but the storm may be much longer than one week.

If you had invested with 3x leverage (daily rebalanced) in the S&P 500 anytime in 1999 or 2000 you would have been down over 90% in 2009 and you wouldn't have broken even until 2014 or 2016.

Well you would have done just amazing (as I pointed out) over the last 5 years. Better than 3x the S&P 500.

I'm not saying you don't have a point, but one would need to look at how it performs over longer periods with more varied market conditions to answer your question.

Interesting that the last year performance was so bad - I think that stock market drop back in March and the general volatility / reshuffling since then must have hurt the leveraged strategy.

You're arguing against a strawman argument that you invented.

I didn't say you would get those crazy returns - merely pointed out that you would have beat the S&P 500 over the last 5 years with the strategy outlined by the parent post.

How well it holds up over a time period that also includes bear markets is another question - you can't just look at a bull market and assume it's representative of all time.

I think a big distinction that retail traders need to come to terms with is that, while yes, technically you can make reasonably good sums of money with various trading strategies of various risk profiles, as one person, so many of them are just not worth the trouble.

If your passion is this sort of thing, by all means, go ahead.

But it's like running a homelab. Yes, you can get pretty decent "savings" (vs running in AWS/DO) but I can guarantee you, you will end up in the basement replugging ethernet cables trying to figure out which one is the bad one while your family and relatives are waiting upstairs, fairly bemused, for you to fix "the internet".

It's possible, but as a person with a life, unless it's your passion, I'd recommend just not. Do the financial equivalent of paying DigitalOcean 5 dollars a month: buy sp500 etfs and sit on them.

I wonder if we can invest in a fund manager who does this strategy. And if it's so good then why do pension funds and endowments not allocate to it typically.

{kind=link}