It's designed to sell option premium on major indices (like the S&P500 or NASDAQ-100) to generate mostly passive income, with a fairly reasonable risk-adjusted return. It uses a combination of strategies that involve selling naked puts and covered calls, which both have the same risk profile, but naked puts tend to have higher premiums.

I briefly looked at the README and code. The strategy is an implementation of The Wheel. Did you backtest the strategy including commissions?

I doubt there is much left after commissions. See [0] for a backtest including commissions and [1] for a blog post from ORATS on how to backtest the strategy using the ORATS backtester.

What many people don't understand about the relatively low-risk options strategies like the wheel or basic covered call selling is that, because they are low risk, they are less lucrative than many simpler strategies.

The financial industry would not just leave that much risk-adjusted return on the table, after all. Just because a strategy is complex does not mean it is lucrative.

I think you must mean that covered calls or the wheel are less lucrative than more complex strategies, unless I'm really missing something. Can't get much simpler than a CC.

The Wheel as a strategy doesn't scale well, though. A good stock for the wheel has relatively low volatility, but with high volume of option interest. These two things are kind of opposed to each other, though. If a stock isn't very volatile, then there isn't much need for large option interest.

Of course there is a lot of overlap where things get interesting.

I think the reason why there aren't a lot of institutions running the wheel et. large. is because it just can't work at the scale they want to operate on. You can probably run the wheel pretty successfully at a million in capital (much larger than I'm used to), but at 10, 100, or 1 billion, it just doesn't work.

And what are they going to do? Pay some guy 200K to generate maybe 200K on a million in capital?

What I mean is that wheeling on SPY is less lucrative than even buying and holding SPY over time, because they are lower risk; see the linked post with backtesting. The past year is not a great example because we have had periods of higher-than-normal volatility.

Of course, you might have better luck wheeling on something with much more implied risk than SPY or cycling through some of the most risky stocks. But depending on where you are in the wheel, you are still yourself assuming risk that can make you lose money (e.g. a collapse in implied risk while you hold the stock).

When you say wheeling works best on a stock with low volatility and high OI, what you mean is that it works best on a security with under-priced risk. I am sure there are actually many funds running strategies based on exploiting over-priced risk premiums. They just have no need to trade options on the open market since they can work with a market maker who can take the other side for them.

Genuine question, does this strike others as immensely off-topic? I'm curious if the parent commenter even opened the link. I'm sure there are applications of generalized knapsack problems (or dynamic programming generally) in options trading, but this isn't it.

If you check their profile you can see they created their account 4 months ago, so they are likely to be new here. No need to be disagreeable to make your point.

The problem is the books don't really tell you. They're written in this mathematical way that kinda obscures how to actually think about them practically. If you're more into math maybe stochastic calc will be just fine for you.

Here we go anyway:

Hull: Futures, Options, and Other Derivatives

Natenberg. Don't recall the name, but this is maybe the closest to practical.

Paul Wilmott, Quantitative finance.

Taleb, Dynamic Hedging. Got a signed copy :)

Also I think it's smart to read about instruments that aren't options, ie don't just cut to the chase. Time value of money, futures, forwards, bonds, swaps, equities. Then vanilla options on all those things, then exotics.

Someone with a strong math background should cut Wilmott and go directly to Shreve: Stochastic Calculus for Finance II (or Björk: Arbitrage Theory in Continuous Time).

What does "strong math background" mean in this context? Would the equivalent of an undergrad degree in math be sufficient, or are we talking about graduate level analysis and stats here?

is standard graduate stochastic calculus course material. An undergrad degree in math usually specializes in a certain track: algebra or analysis. The analysis background would be a closer fit as the material is focused on the continuous applications (not HFT) and likely have covered the introductory measure and probability theory material. The finance portion focuses on the arbitrage-risk neutral model that is at least a semester worth a material.

Interesting comment about the math. For my physics degree, a lot of times it was easier to think about things once I understood more of the math. I’ll see how it goes here.

Generally speaking, a seller of naked puts is looking to supplement income via a stock they are willing to own at a lower level. If you are not willing to take delivery, it is probably better to sell a vertical spread so that there is a built in stop out. Here I'm speaking of transactions of a reasonable premium amount, not 5 or 10 cents.

While it is true that the upside is unlimited against a naked call (and the downside is 0 on a naked put), naked puts suffer from systemic risk that calls for all intents do not. Both are subject to news/events specific to the company in question, but the risk of the short call running away from you because the market had a +20% day are well, fleeting. On the other hand, unexpected economic news, politcal/military events, liquidity issues, etc can tank the entire market 10, 20, 30% and have numerous times. A rise of similar magnitude, to my knowledge, has only happened after market crashes (so you would then be alert to the upside risk).

What? If the stock goes lower than the strike price, the downside on a naked put is the difference between strike price and market price. You will be forced to take delivery of the stock at the strike price when you could have bought it for market price if you hadn't written the option.

This is why skew exists, and should not deter anyone. The vast majority of people should buy a 20-30% dip, and so the fact that 99% of the time you're not going to be assigned means that it's a good idea in most scenarios.

I suggest most retail to be short straddles against a core underlying position for yield enhancement. Yes, over a number of decades you will have something go against you, but under the current monetary and fiscal regimes, you should be hoping for the day that you can buy the dip or sell the rip via a systemic short vol overlay.

The problem with traditional retail being short naked puts is they generally do not have a pool of cash sitting on the sidelines to absorb margin calls and/or buy (if assigned). Likewise, buying in a tanking market on margin entails additional risk that needs to be well considered before hand.

Selling straddles or strangles against a long position in a stock that you do like is reasonable play, but there needs to be a full understanding of how vol and time decay can effect the value of the entire position up to maturity and a recognition that nobody is getting assigned/called early excepting unique circumstances (ie, high dividend stocks)

For those reasons, I'd only suggest these types of trades to fairly well capitalized retail investors and those who have taken the time to gain a basic understanding of equity options and the use of margin. In proper hands, these can be very rewarding trade ideas/techniques.

> The vast majority of people should buy a 20-30% dip, and so the fact that 99% of the time you're not going to be assigned means that it's a good idea in most scenarios.

So "people should buy a 20-30% dip" but should not be invested already? Because if they are, selling puts may not be a good idea.

I think what he is suggesting is that historically buying after a 20% or more sell-off leads to outsized gains in the US market.

That does not preculde already being invested as sitting on the sidelines waiting for such a move can be self defeating (the market rises 50% then drops 30% dramatically you would still be better off to have bought day one).

If you sell puts and are assigned, it may or may not happen at the optimal post crash price, but you will still be adding to your long at a much lower level. For instance, you sell a 30 put when the market is at 45. There is a great sell off, you are assigned when the underlying is trading at 25. You own at 30 less whatever premium you received, likely above 25. Certainly not the end of the world, but investor psychology is such that some people will be upset after the fact if they are paying more than current market price.

However, if you are not assigned you'll be pocketing those premiums as added income. But that is also another risk with naked puts - the market sells off but well before expiration and then rises again. You would miss the chance to buy unless you make the decision to take back the short puts at a loss and buy the cash at the now lower price. Again, you'll likely be paying net more than just having parked the cash and waited.

So naked puts may not be the best strategy if you know you absolutely positively will want to buy at a certain price, no matter what.

The point is that if you're already fully invested you don't have money to buy those additional shares. And if you didn't want the leverage before, commiting to take on leverage later may or may not be a wise thing to do.

It may make sense if you had dry powder waiting for a correction. But at that point you are forced to buy (and as you say it may be at a higher price that the prevailing one in the market). You get premiums but you lose flexibility.

> Generally speaking, a seller of naked puts is looking to supplement income via a stock they are willing to own at a lower level.

The problem is that they may be willing to own at a lower level today. But it may happen that when they have to own it the price is lower for a good reason.

Selling a deep in the money put behaves like owning the stock (probably with margin, but it depends on how many puts you are selling compared to your reserves of cash and short term "safe" bonds) except that you are capping your gains.

The further towards out of the money you go the more it behaves like picking up pennies in front of a steamroller. But an interesting quirk of selling puts compared to calls is that the downside is limited. The stock can't go below 0.

That gives me a good intuitive picture. I'd really love a basic online simulator where I can plug in portfolio characteristics (eg percent of calls Vs puts, ATM Vs OTM) and simulate an equity curve over the last ten years. I could build my own of course but I think a tool like this would be generally useful for investors.

I did make my own option trading algo which is similar to the one in the Git Hub repo (but I used Scala, which gave me additional returns, jk :) ). Return totally depends on the delta of the options you write and the option symbols in your basket. Mine could be configured to be between 10-100+%. The higher the return the more volatile.

The idea of using multiple symbols like SPY and TLT is to reduce the tail risk. But in the end there is still tail risk like for example in the crash of 2015. Making the strategy delta neutral with hedging could improve it but I never completed that part.

There is an interesting book with all the math by Euan Sinclair about option writing and how to minimize the risk if you are interested.

Another way to reduce tail risk when selling options is to simply hedge with a protective call/put at a higher or lower strike respectively. Sufficiently far off strikes will have minimal impacts on returns while reducing tail risk.

If you want to go heavy duty into it I recommend the Hull book (options, futures and other derivatives) but for your purposes the investopedia articles are enough.

Basically naked puts means you’re selling downside insurance so if the stock crashes you eat the loss. Covered calls mean you sell upside risk but have the stock so if it goes up you make a little.

Hull is a great book and is not too heavy on the math. However, for someone just getting their feet wet, Options as a Strategic Investment by MacMillan is a classic.

The "tail" in tail risk referes to the tails of a probability distribution. A normal distribution has "thin" tails. The probability of huge outliers is pretty low.

If you have tail risk, then it means you have a decent chance of losing a lot more money than the typical variation. Your returns might look like +1.1, +0.9, +1.2 +1.05, -3. So your profit is pretty predictable with little variation, until suddenly you lose a lot of money.

The only book you should read is John Bogel's. Do what he says like Goldman partners, Bank of America senior executives, almost every economist does with their money and stick it in low cost diversified mutual funds.

Or you can learn stochastic calculus and end up in the same place once you realize half of all active traders do worse than the market, before fees.

None of the kinds of people you listed are good at trading (esp economists). From experience, professional traders do tend to use passive indices for part of their PA, but also actively trade a portion.

But you're right in that if you don't have a passion for it, you'll never be able to truly outperform spy on a risk adjusted basis. However, if you do have the knowledge and the passion, I definitely think you can.

Investing is personal, and just holding spy doesn't fulfill everyone's objectives.

Here's an example of a strategy that outperforms spy in most cases: 1/3 of your portfolio goes to upro (3x leveraged spy) and 2/3s goes to a bond fund/etf. As long as the bond etf returns above the upro expense ratio (~1%), you will outperform. From my backtests, this strategy will earn you an extra 1-2% return a year, while also having a slightly higher risk adjusted returns.

I list the above as a great example because it's the kind of strategy that is great for a PA: easy to manage, doesn't require babysitting, and backed by solid academic research. When people think active vs passive, they think actively trading single stocks vs just holding an index. My point is that you can use some quant-lite strategies that tilt your portfolio to eek out a little return. You don't have to be trading everyday or even holding anything except ETFs.

While I always preached just buying the S&P one risk i've been seeing with it is if, a majority of investors just buy the S&P index, since the index is market cap weighted, it would just make the largest stocks in the index more expensive.

This would make the stocks that have less weight in the index or stocks outside the index relatively cheap and obviously offer better returns.

Assuming the amount of tradable shares for each stock is proportional to the free float capitalization (which is not a particularly good assumption), each stock in the index should be pushed up by the same amount, since the weight of each stock in the index is proportional to the market cap of the stock. I don't think this is actually true (i.e the number of shares on the market is not proportional to the market cap), which would imply that some share prices would be affected more than other. Do higher weight stocks in spy get pushed up more? I don't know. But it is certainly possible.

With respect to the stocks just outside the index, I think you could argue that they are probably undervalued and thus should offer better returns. This is what an academic would say. However, the actual reality could be a lot different: if returns are dominated by flows instead of fundamentals (like they are now), maybe going with the crowd is the best investment strategy. Or maybe not, I haven't done the research.

One thing that every market professional is worried about right now is just how dysfunctional valuations and returns seem to be in the modern era. Stocks seem to go up for no reason and returns have been disconnected from both fundamental and quantitative risk premia.

What I can say for sure is that we are in a period of intense change in the financial system. No one knows what the future of finance will look like, 10 years, 20, or 30 years out. Will crypto defi take over? Will traditional finance be disrupted? No one knows, but it is certainly an exciting time to work in the capital markets!

Sorry, I'm using risk premia incorrectly (quant equities isn't actually my thing).

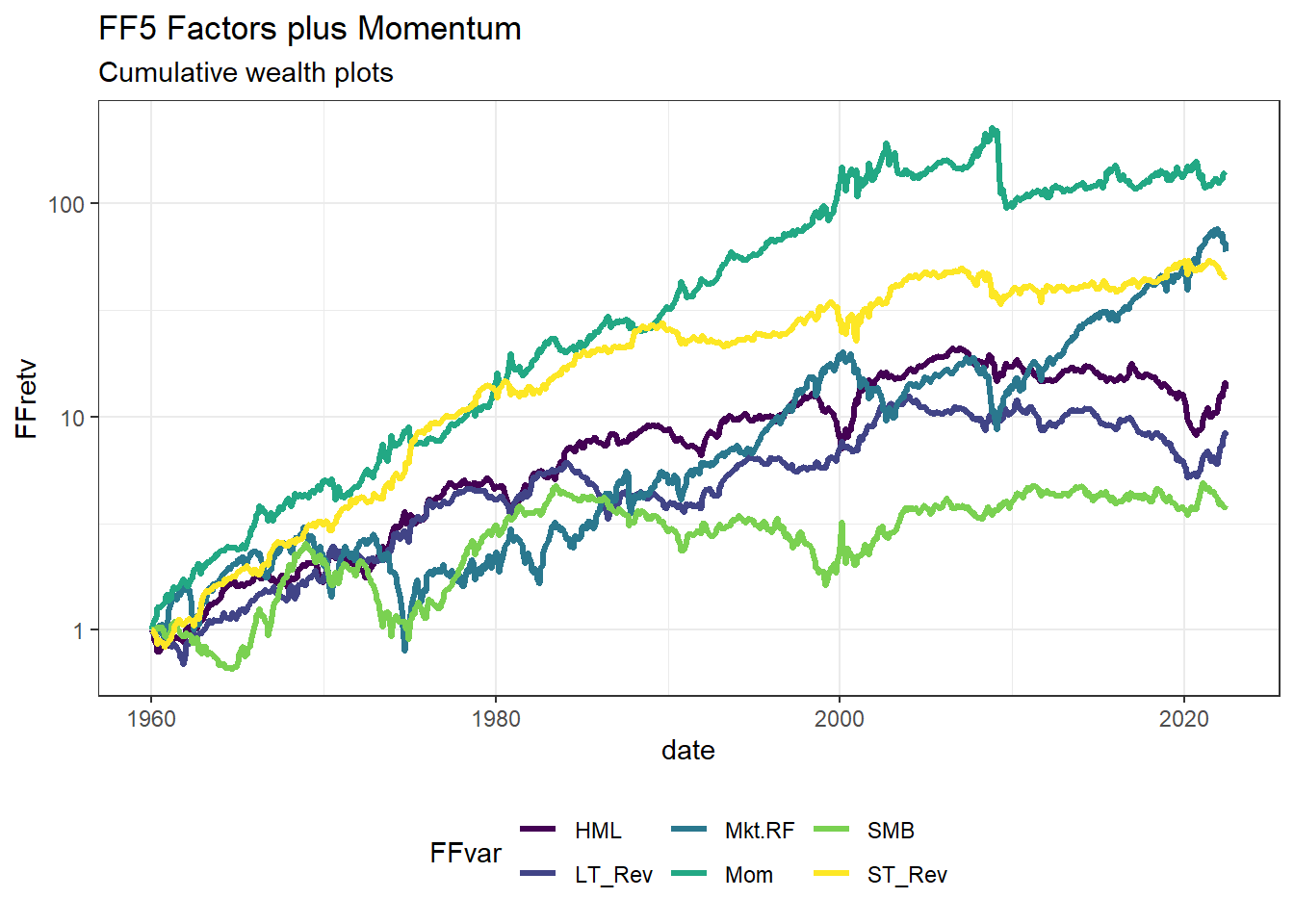

What I mean is that I don't believe smb truly delivers superior risk adjusted returns. For example, I believe the betting against beta factor (BAB) does, while smb does not.

We agree then, the size factor has not been really outperforming since it was introduced in the nineties. Maybe the drivers of the outperformace were things like transaction costs and lack of information which are less of an issue in recent times.

For what it’s worth, the value factor is not doing well recently either...

by beta slippage you mean volatility drag? On a risk adjusted basis, upro is definitely a loser due to volatility drag and high expense ratio. However, you can easily calculate optimal leverage ratio in order to maximize the geometric growth of your portfolio. The equation is:

lev = E(r) / Var(r)

So if the expected return is 10% and the expected volatility is 10%, optimal leverage to maximize geometric growth is 10x.

This of course is much too high and the risk of losing everything due to excessive kurtosis and downside skew is very high. Like the everything else in finance, fundamental sin of that formula is assumption of the log normality of returns.

However, is 3x too high for the long term? I dunno, but over long time periods, a pure 3x leveraged spy portfolio is going to outperform significantly. The problem is most people will be unable to weather the storm as you can easily lose half of your money in a week.

I wouldn't hold pure spy 3x and wouldn't exactly recommend it, but from a mathematical perspective it is a defensible (as in, you can make cogent arguments for it) long term investment.

On the other hand, I would probably recommend 1.5x lev or possibly even 2x lev to certain people.

As a quant, I approach these things like leverage from a mathematical perspective. It's important not to have an emotional reaction. There are very smart people running books that have 10x leverage but you would never be able to guess by looking at their volatility. It's all about the factor exposures, net delta, etc.

For example I've seen 15x leveraged delta neutral books that have absolutely insane Sharpe ratios (>15) and annualized volatility of less than 5%.

> However, is 3x too high for the long term? I dunno, but over long time periods, a pure 3x leveraged spy portfolio is going to outperform significantly. The problem is most people will be unable to weather the storm as you can easily lose half of your money in a week.

You don't define "long time periods" but the storm may be much longer than one week.

If you had invested with 3x leverage (daily rebalanced) in the S&P 500 anytime in 1999 or 2000 you would have been down over 90% in 2009 and you wouldn't have broken even until 2014 or 2016.

Well you would have done just amazing (as I pointed out) over the last 5 years. Better than 3x the S&P 500.

I'm not saying you don't have a point, but one would need to look at how it performs over longer periods with more varied market conditions to answer your question.

Interesting that the last year performance was so bad - I think that stock market drop back in March and the general volatility / reshuffling since then must have hurt the leveraged strategy.

You're arguing against a strawman argument that you invented.

I didn't say you would get those crazy returns - merely pointed out that you would have beat the S&P 500 over the last 5 years with the strategy outlined by the parent post.

How well it holds up over a time period that also includes bear markets is another question - you can't just look at a bull market and assume it's representative of all time.

I think a big distinction that retail traders need to come to terms with is that, while yes, technically you can make reasonably good sums of money with various trading strategies of various risk profiles, as one person, so many of them are just not worth the trouble.

If your passion is this sort of thing, by all means, go ahead.

But it's like running a homelab. Yes, you can get pretty decent "savings" (vs running in AWS/DO) but I can guarantee you, you will end up in the basement replugging ethernet cables trying to figure out which one is the bad one while your family and relatives are waiting upstairs, fairly bemused, for you to fix "the internet".

It's possible, but as a person with a life, unless it's your passion, I'd recommend just not. Do the financial equivalent of paying DigitalOcean 5 dollars a month: buy sp500 etfs and sit on them.

I wonder if we can invest in a fund manager who does this strategy. And if it's so good then why do pension funds and endowments not allocate to it typically.

That is the normal behaviour for commodities. It's arguably reasonable that Bitcoin behaves more like a commodity than a stock, at least so far as anything is arguably reasonable in the realm of cryptocurrency.

But maybe strategies involving puts will become more successful if we can convince more of the HN Bitcoin naysayers to sign up for LedgerX and put their money where their mouth is. :)

There's a fantastic quote in the book about the LTCM fiasco ("When genius failed") about how academics always want to short volatility because they have view of how society "should be" and it is not very volatile. IIRC, the quote was by some old grizzled options trader who used to have the same view but had been bitten often enough to internalize that volatility is much more common than beginners think.

> Copyright (C) 2020-2021 Terence Kelly. All rights reserved.

did you happen to get the author's permission to put that up? I don't even like IP law that much, but its funny to me how much no one gives a shit. This was a crime, albeit a silly and small one.

Copyright infringement is not a crime in and of itself. It's only criminal when it's done for commercial purpose with financial gain which is clearly not the case here.

> Copyright infringement is not a crime in and of itself. It's only criminal when it's done for commercial purpose with financial gain which is clearly not the case here.

US Copyright laws, sure, this statement is correct. In some countries (especially in Europe and Asia) however, this is pretty much the opposite.

(Point noted however that Mr. Kelly is probably American, which assuming you're American will be subjected to U.S. IP laws, especially DMCA provisions. Since that this is unprotected, DMCA circumvention is out and this infringement would be only a crime if this was specifically filed in court, and even them it might be argued that this is more of a civil lawsuit than a criminal lawsuit.)

You're ignorant pertaining to what you are talking about.

https://www.dictionary.com/browse/crime

a crime is supposed to be offensive. The only thing this law being broken is offensive to is copyright holders who are one, punishing people for promoting their content, and two, the media is protected for an obscene amount of time to where usually eventually the ip is purchased from someone who put no effort into the art and is only interested in making money. To me, THAT is a crime.

Reading more about things you haven't read about before will increase your total knowledge and therefore make you better off in a holistic sense, yes. In a purely monetary sense, no it will probably not have any effect on your life.

I was making the gamble that people who compulsively ask "Will it make me better off?" without having read the article are not yet at the point where they've hit the diminishing returns on additional knowledge.

Your statement is correct though, username checks out as well.

The Vickery Auction was pretty much the de-facto auction type in adtech realtime bidding.

It's since been replaced with standard first-price auctions for reasons I don't fully understand, but I assume it was because websites misunderstood bid prices and though they were being ripped off.

Just asking anybody figured out, how to find high low for a period of time. Say in a period of 6months, starting from a initial point, next point could be a high or low, if high, program needs to find next lowest point and afterward, it needs to find highest amd continues to do so in zigzag. For low it's vice versa.

I think what you are asking is given a time series (x_0, x_1... x_n), what is the 6 month high (or low) on day i? In other words you want the max (or min) of the sub series (x_{i-180},x_{i-179}... x_i).

x_0 is obviously the 6 month high at day 0 (since there is no previous data). If x_1 > x_0 then x_1 is the new 6 month high so we can discard x_0 on day 1. If x_1 < x_0 then x_0 is still the 6 month high on day 1, but we cannot discard x_1 because it might become the 6 month high when x_0 expires on day 181. So we need to maintain some sort of data structure of potential 6 month highs such that we can lookup the current high and remove these highs as they expire or get replaced. The easiest way to do this is with a list of pairs [(x_i1, i1), (x_i2, i2)...] sorted by increasing x_i. Because it is sorted, the current high is always found on the element closest to the end of the list. Furthermore when a new element (x_k, k) is added, it replaces all the elements which come before it (thus they can be removed). As a corollary, because the newest element is always added to the back (after removing what's in front of it), the list is also sorted by order of expiry (with the oldest (x_i,i) at the end). Start with an empty list and i = 0

Find the sorted insertion point in the list for (x_i,i).

Remove everything prior to the insertion point.

Insert (x_i, i) at the start of the list.

If the element at the end of the list (x_n, n) is expired (n < i+180) then remove it.

The 6 month high on day i is found in the element at the end of the list. Store this in a new series h_i.

Increment i by 1 and repeat.

This method trivially works for finding the 6 month low as well.

You can do it in a single pass fairly easily. Loop over the rows of data. Store the current high to low, as well as the largest high to low since inception. If the current exceeds the largest since inception, simply replace it. Should be about 30 lines of code.

{kind=link}

It's designed to sell option premium on major indices (like the S&P500 or NASDAQ-100) to generate mostly passive income, with a fairly reasonable risk-adjusted return. It uses a combination of strategies that involve selling naked puts and covered calls, which both have the same risk profile, but naked puts tend to have higher premiums.